This is an overview and assessment of a product category, the African fintech super-app, based on publicly documented features and how these products are used, rather than a hands-on review of a single app.

Open the home screen of almost any leading African consumer-fintech app today and you will see the same ambition: it no longer wants to do one thing. Payments sit beside transport, beside bill payments, beside shopping, beside savings. The model has a name borrowed from Asia, the super-app, and across the continent companies from Nigeria to Côte d’Ivoire are racing toward it. This is an assessment of how that race is going.

Why everyone wants to be the everything app

The logic is sound and comes straight from Asian platforms like WeChat and Grab. Acquiring a user is expensive, so once you have their trust and their payment details, every additional service you can offer them is cheap incremental revenue, and every service makes them less likely to leave. In African markets, where many people skipped desktop computing and traditional banking entirely, the phone is the primary financial tool, which makes a single app that handles money, movement and commerce genuinely useful rather than just convenient.

Different companies approach it from different starting points. Some begin as ride-hailing or delivery and add payments. Some begin as mobile money or remittances and add commerce. Some begin as classic fintech and bolt on transport and shopping. The destination is the same: be the daily app the user opens without thinking.

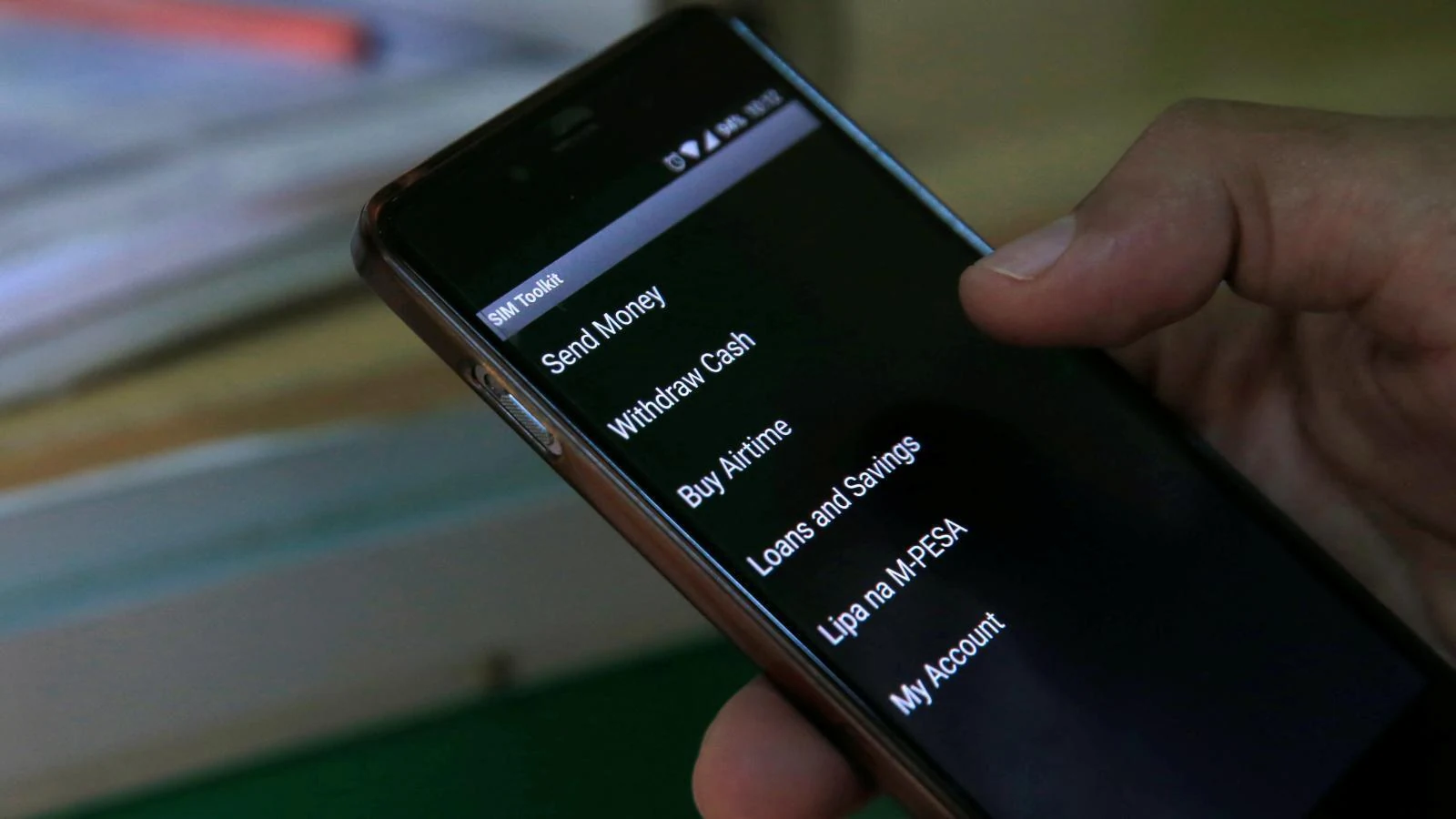

What works

When it works, it works well. A user who can pay a merchant, send money to family, top up airtime, settle a utility bill and order a ride without leaving one app experiences real convenience, especially where the alternative is juggling cash, bank queues and several disconnected services. The best of these apps lean on a genuine strength: deep local payment integration that foreign apps cannot easily replicate, and a low-fee, mobile-first design that suits markets traditional banks underserve. For the companies, the data exhaust from all that activity is gold, enabling credit scoring and embedded lending that would otherwise be impossible.

What does not

The failure mode is just as clear. Many super-apps become bloated, cramming in features that few users actually want in pursuit of a strategy that matters more to the company than the customer. A transport app that adds mediocre shopping, or a payments app that adds a half-built marketplace, often ends up worse at its core job without winning the new one. Reliability suffers as complexity grows, and in markets with patchy connectivity and entry-level devices, a heavy, feature-stuffed app is a liability.

There is also a trust dimension. Concentrating someone’s money, identity and daily transactions in one app raises the stakes of any outage, breach or account freeze. When the everything app goes down, it takes everything with it.

The verdict

The super-app push is rational, and in the strongest products it delivers real value to users who genuinely benefit from consolidation. But too often the strategy serves the company’s growth ambitions more than the customer’s needs, producing apps that do many things adequately and nothing exceptionally. The winners will likely be those that earn the right to expand, nailing one core service so well that users want more from them, rather than those that bolt on features to flatter a pitch deck.

For users, the practical test is simple: does the app make your financial life easier, or just busier? For the continent, the super-app race is worth watching less for the buzzword than for what it reveals, that the real prize in African fintech is not any single feature, but becoming the trusted, everyday rail through which money moves.

This article is for general information and is not financial advice.