African startup funding is moving closer to the $1 billion mark for the first half of 2026, but the market underneath that number is becoming narrower.

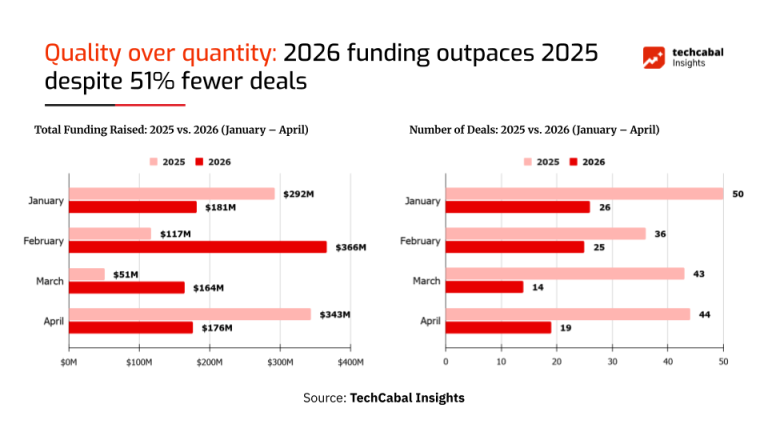

According to TechCabal Insights, startups across the continent raised $887 million between January and April 2026, up from $803 million during the same period in 2025. On the surface, that looks like a healthier market. But the number of disclosed transactions fell from 173 deals in January–April 2025 to 84 deals in the same period this year.

That is the real story.

Capital is still moving. It is just moving into fewer companies.

For founders, this is a mixed signal. Investors have not disappeared, but they are becoming more selective. For operators, the implication is sharper: fundraising is not only about being in the right sector anymore. It is about showing stronger traction, cleaner numbers, and a clearer path to capital-efficient growth.

A bigger number with fewer deals

The headline figure is strong. At $887 million in four months, African startups need roughly $113 million across May and June to cross $1 billion in the first half of 2026. TechCabal Insights described the funding market as one that is choosing “quality over quantity,” with fewer transactions carrying more of the total capital.

That phrase captures the shift well, but it also needs a little unpacking.

A market can look healthy by total funding and still feel difficult for most founders. If more money is going into fewer rounds, the average headline may improve while access to capital becomes tighter for early-stage companies. The visible market looks active. The founder pipeline feels more constrained.

This is what appears to be happening.

The decline in deal count suggests investors are concentrating capital around companies they see as more resilient, more proven, or better positioned to manage difficult operating conditions. That may include startups with stronger revenue, better margins, clearer repayment capacity, or infrastructure-like business models.

It also means weaker companies, vague models, and traction-light startups will find it harder to raise on narrative alone.

The market is not dry. It is more selective.

The return of larger rounds

TechCabal Insights reported that capital concentration is especially visible in larger funding brackets, including the $10 million to $49 million and $50 million to $99 million ranges.

That matters because large rounds do more than lift the total funding number. They shape market psychology.

When a few companies raise big rounds, it can create the impression of broad recovery. But the healthier question is not whether a handful of companies can raise. It is whether strong companies across stages can access the right kind of capital.

A venture market needs both. It needs later-stage companies capable of absorbing larger cheques, and it needs enough early-stage funding to keep the pipeline alive.

If the top of the market gets stronger while the bottom thins out, the continent may see more capital concentration but fewer new venture-backed winners. That would be a quieter problem than a funding crash, but still a serious one.

Debt is becoming harder to ignore

One of the more important signals in the report is the role of debt.

TechCabal Insights notes that debt financing has become a major driver of the 2026 funding total, especially in sectors such as climate tech and fintech. In February 2026, debt accounted for $235 million, almost twice the level of equity funding for that month, according to the report summary.

This shift makes sense.

Debt can work well for companies with predictable cash flows, asset-heavy models, credit products, energy infrastructure, receivables, or financing needs that do not fit cleanly into equity rounds. For founders, it can reduce dilution. For investors and lenders, it can offer clearer repayment logic than waiting for a future exit.

But debt is not free money. It introduces repayment pressure. It can strengthen a company with disciplined cash flow, but it can also expose weak unit economics faster than equity.

That is why the growing role of debt should be read carefully. It may show maturity in parts of the market. It may also show that some companies are raising capital in forms that demand tighter financial discipline.

Debt rewards discipline. It punishes wishful thinking.

What this means for founders

For African founders, the message is not to panic. It is to adjust.

The funding market is still open, but the bar has moved. Investors are asking harder questions, and the answers need to be clearer than they were during the easier funding years.

Founders raising in this market need to understand what kind of capital fits the business. Not every company should raise venture capital. Not every company should take debt. Not every business needs to scale at the pace investors want.

The sharper question is: what does the company actually need capital for?

If the money is for customer acquisition, the founder must show that acquisition leads to retention and revenue. If it is for expansion, the founder must show that the next market behaves like the current one, or explain why it does not. If it is for lending, energy, logistics, or other capital-heavy operations, the founder must show how cash cycles, repayment, defaults, and margins work.

A better funding story in 2026 will not be built on market size alone. It will be built on execution quality.

What this means for investors

For investors, the thinner deal count may look like discipline. But there is a risk in over-concentration.

If too much capital flows to a small number of companies, the market may miss important early-stage opportunities in less obvious sectors, cities, and countries. That is especially relevant in Africa, where strong businesses are not always built in the most visible markets and do not always look like Silicon Valley-style venture companies in their early years.

The best investors will need to balance caution with curiosity.

They will need stronger diligence, but not lazy pattern matching. They will need to look beyond familiar sectors and ask whether overlooked companies are building with better economics, deeper local insight, or more patient growth models.

A selective market can improve funding discipline. It can also become too narrow if investors only fund what already looks safe.

The early-stage question

The biggest concern is what happens to companies before they are ready for larger rounds.

A continent cannot build a stronger late-stage market without a healthy early-stage pipeline. If seed and pre-Series A funding become too constrained, fewer companies will survive long enough to become growth-stage candidates.

This is where accelerators, angel networks, local funds, corporate venture arms, and development finance institutions still matter. The market needs more than headline capital. It needs stage-appropriate capital.

Early-stage founders often do not need enormous cheques. They need enough capital to test distribution, prove demand, refine the product, and build credible operating data.

If that layer weakens, the funding market may look impressive in total value while becoming less fertile underneath.

The sectors to watch

The current funding pattern suggests investors are paying attention to sectors where revenue, infrastructure, or repayment logic is easier to understand.

Fintech remains important because money movement, credit, payments, and financial infrastructure still sit at the centre of African commerce. Climate and energy companies are also attracting capital because many of them combine infrastructure need with measurable demand.

But the important point is not simply sector preference. It is business-model clarity.

Investors are likely to favour companies that can explain how they make money, how they retain users, how they manage risk, and how capital turns into growth.

That creates pressure on founders to move away from broad claims and toward sharper operating proof.

What to watch next

The next two months will show whether African startup funding crosses the $1 billion mark in the first half of 2026. Based on the current figure, the market only needs about $113 million more to get there.

But the more important question is not whether the market crosses a headline number.

The better question is what kind of market is being built.

If the next wave of funding produces stronger companies, better capital structures, more disciplined growth, and deeper infrastructure, then the smaller deal count may be a sign of maturity.

If it produces a market where only a few companies can raise while early-stage founders struggle for oxygen, then the recovery will be thinner than it looks.

For now, the signal is clear: African startup funding is not frozen. It is concentrating.

Founders can still raise. But the market is asking for more proof.