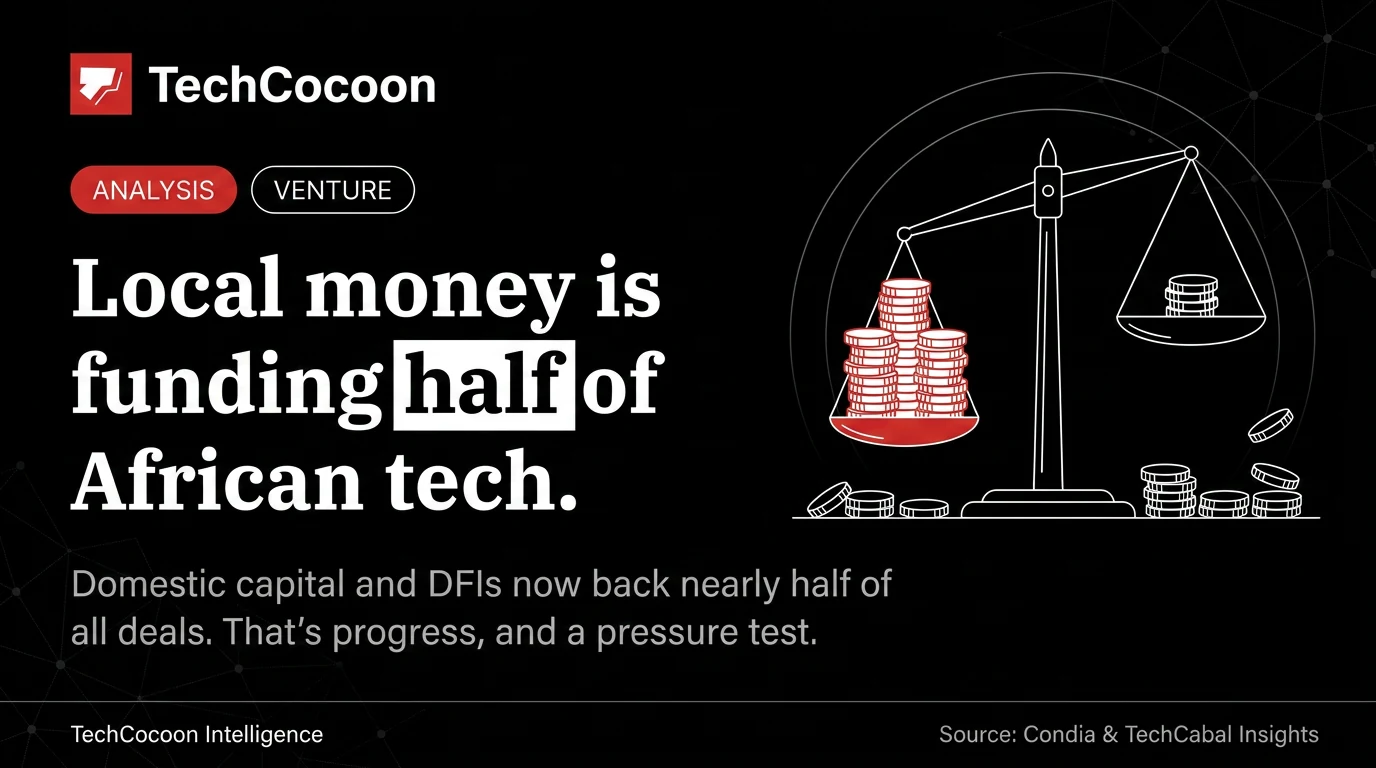

The encouraging line in the latest data is easy to miss under the totals. African startups have raised roughly $900 million across 74 equity deals in the first five months of 2026, and on recent watchlists close to half of that capital is coming from local sources. After years in which the ecosystem’s fortunes tracked the mood of US and European funds, homegrown and regional capital now carries something near half the load. That is a genuine structural shift, and the most durable kind of progress this market can make.

Why it matters, beyond the cheerleading

The case for local capital is not sentiment. Capital raised from domestic, regional and DFI-linked sources is far less exposed to the swings of global venture sentiment that whipsawed African startups from 2022 onward; when foreign money retreats, ecosystems that depend on it stall, while those with a homegrown base keep moving. It also keeps more of the upside, and the decision-making, on the continent. This publication has argued before that a smaller round led by a committed local investor is often structurally more interesting than a larger one led by a foreign fund passing through, because local, repeat capital tends to bring follow-on capacity and networks that a one-off cheque does not. The current numbers are that thesis showing up in the aggregate.

The pressure test on our own conviction

Here is where intellectual honesty has to bite. The same discipline that makes this publication skeptical of foreign-led mega-rounds, show the instrument, show the disclosed volumes, distrust vanity metrics, has to apply with equal force to the local-capital deals it is inclined to celebrate. The risk in a house view is grading the capital you like on a curve.

And the local and DFI-led rounds defining this stretch are frequently the ones with the thinnest disclosure: undisclosed amounts, bridge facilities reported without figures, traffic offered in place of transaction value. A movement is only as healthy as its evidence, and “nearly half of funding is local” is a watchlist composition, not an audited fact; it can be reshaped by a single large deal or a change in what trackers count. TechCocoon Intelligence reads the local-capital rise as real and important, and insists on holding it to the same standard as everything else: enthusiasm for who is writing the cheque is not a reason to ask fewer questions about what the cheque bought.

There is a second pressure test underneath the first. Much of this capital is arriving as debt and structured instruments rather than equity, a shift that rewards companies with revenue and collateral and does little for the unproven, pre-revenue founder, exactly the stage where early risk capital has thinned most. So “local capital is rising” and “early-stage equity is shrinking” are both true at once, and they pull in different directions.

Which leaves the question worth sitting with rather than resolving: is the rise of homegrown capital building a broader, more resilient base for African tech, or is it concentrating a maturing market around fewer, better-financed, better-collateralised companies while the riskiest and most original founders find the door narrower than before? The honest answer is that it is doing both, and which one dominates over the next two years depends less on how much local capital shows up than on whether it is willing to fund the unproven, and to disclose what it funds.